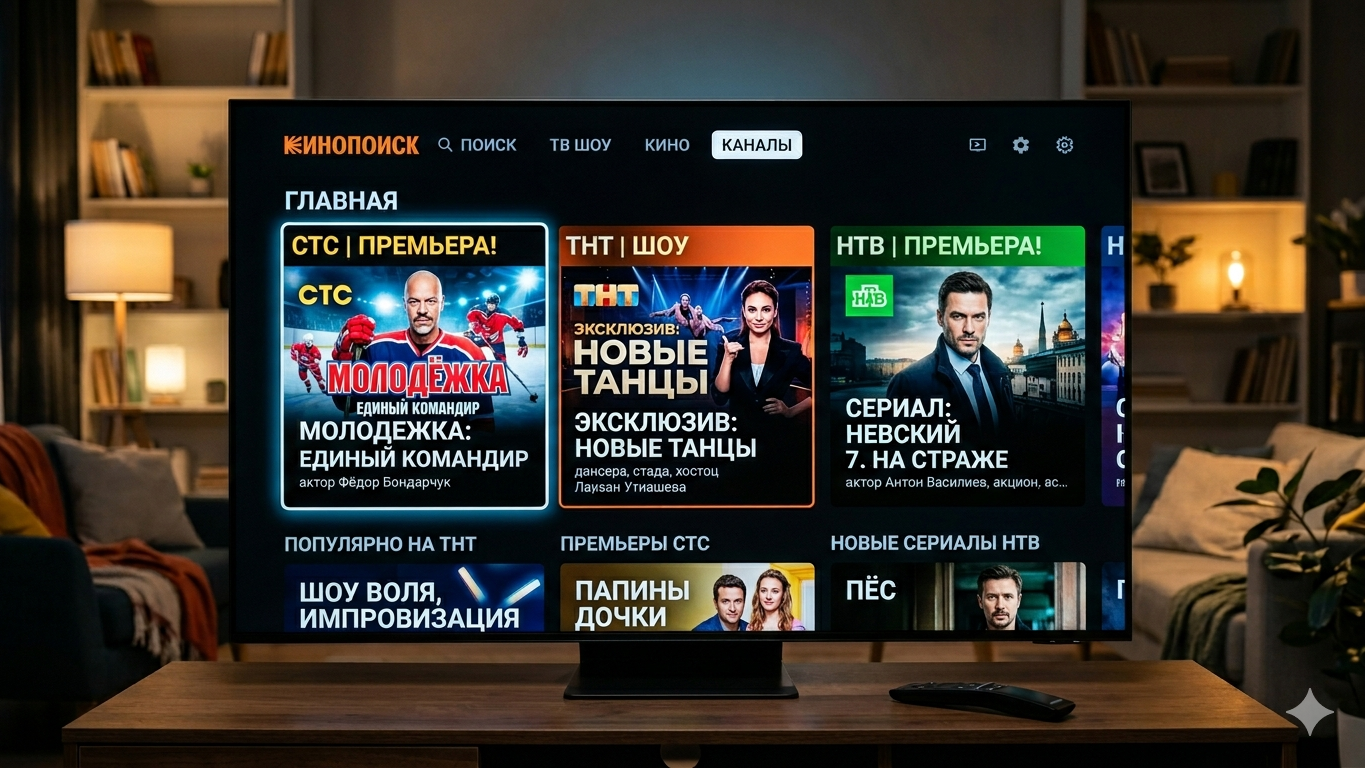

▶️ Online cinema market expands despite a lack of new hit series

The Russian online cinema market is showing paradoxical results. According to Daria Pugacheva, Director of the Research Department at Gazprom-Media Holding, streaming platforms are rapidly boosting revenues even as they lose their primary selling point: exclusive series.

Revenues rise as exclusivity falls

By the end of 2025, streaming revenues soared by 40%, reaching between 178 billion and 206 billion rubles, while the number of paid subscriptions jumped from 58 million to 75 million. However, a content lull lurks behind these impressive figures. In the first quarter of 2026, the market saw the release of just 19 original live-action series, compared to 24 during the same period last year. Viewer interest in new releases, as measured by Yandex Wordstat, plummeted by 40%, and the year has yet to produce high-profile premieres on the scale of past hits like Lilies of the Valley (Landyshi) or Outsource (Autsource).

Two survival models

To maintain profitability margins, industry players have split into two distinct strategic groups:

- The Ecosystem Model: Services achieve growth through multi-service bundling and price hikes. In 2026, the subscription fee for Kinopoisk (as part of Yandex Plus) rose to 499 rubles, Okko (via SberPrime) raised its price to 399 rubles, and Wink increased its rate to 349 rubles. Similar ecosystem-based retention mechanisms are utilized by Kion (MTS) and Wink (T2).

- The Partnership Model: Platforms lacking the backing of tech or telecom giants are joining forces. Premier is banking on synergies with Rutube; Start has launched joint affiliate programs instead of traditional licensing deals; and Ivi is combating subscriber churn through flexible offers and a joint subscription package with Start.

How platforms cut content costs

Instead of funding risky and expensive productions, streaming services have pivoted to crisis-management tools:

- TV Co-productions and the Abandonment of Exclusivity: Projects are now co-financed alongside television networks. The NTV channel is the most active player here, with five joint projects including The Tunnel (Tonnel) and Black Sun 2 (Chernoye Solntse 2). Furthermore, films are increasingly debuting simultaneously on multiple competing platforms.

- Safe Sequels: The first quarter of 2026 saw the release of 9 sequels to well-known series, up from 6 in the previous year. Producing a sequel is more cost-effective, as it leverages an pre-existing, loyal audience base.

- Purchasing Ready-Made TV Content: Shows and series from federal networks—such as Treshka and Mr. Nail (Mister Nogot) from CTC, alongside projects from TNT and Russia-1—are being acquired en masse by platforms, consistently dominating viewership charts. This strategy allows services to populate their content grids at a low cost.

- Reduced Advertising Expenditures: Online cinemas have cut their TV advertising inventory by 40%. Instead of promoting specific series—a segment whose share in ad spending dropped from 59% to 33%—streamers are now marketing ecosystem subscriptions, sports broadcasts, and their general libraries.

Conclusion

The market is successfully generating cash, but this momentum is driven by price hikes, strategic cooperation, and aggressive cost optimization rather than new creative breakthroughs.

Source: AdIndex

World news